bankruptcy is a legal process that allows individuals to eliminate or repay their debts when they are unable to meet their financial obligations. There are different types of personal bankruptcy, each designed to address specific situations. The most common types of personal bankruptcy in the United States are Chapter 7 and Chapter 13 bankruptcy.

Table of Contents

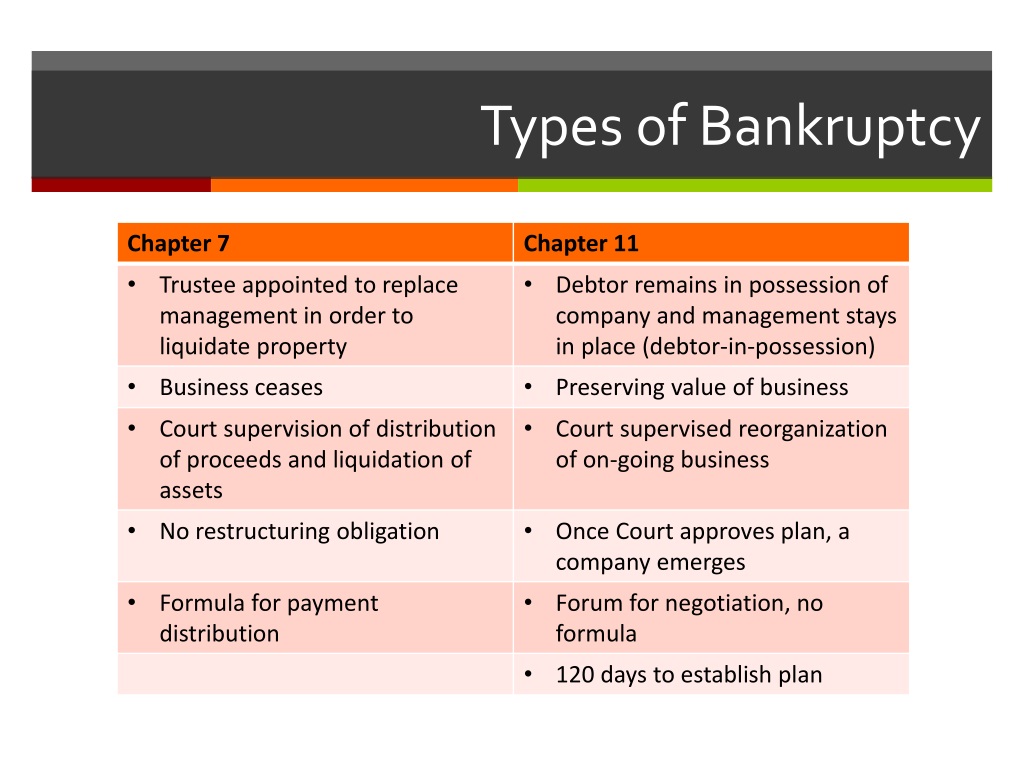

Chapter 7 Bankruptcy

Chapter 7 bankruptcy, also known as “liquidation bankruptcy,” is suitable for individuals with limited income and significant unsecured debts, such as credit card debt or medical bills. In this type of bankruptcy, a trustee is appointed to sell non-exempt assets to repay creditors. However, many states have exemptions that protect certain assets, such as a primary residence, vehicle, or personal belongings. Chapter 7 bankruptcy typically lasts for a few months and provides a fresh start by discharging most unsecured debts.

Chapter 13 Bankruptcy

Chapter 13 bankruptcy, also referred to as “reorganization bankruptcy,” is suitable for individuals with a regular income who want to repay their debts over time. This type of bankruptcy involves creating a repayment plan that spans three to five years, allowing debtors to catch up on missed payments while keeping their assets. Chapter 13 bankruptcy is often chosen by individuals facing foreclosure or those with significant secured debts, such as a mortgage or car loan.

Chapter 11 Bankruptcy

Chapter 11 bankruptcy is primarily designed for businesses, but it can also be used by individuals with substantial debts. It allows debtors to reorganize their finances and develop a plan to repay creditors over time. Chapter 11 bankruptcy is a complex and expensive process, typically used by high-income individuals or those with extensive assets.

Chapter 12 Bankruptcy

Chapter 12 bankruptcy is specifically designed for family farmers and fishermen. It provides a reorganization plan similar to Chapter 13 bankruptcy but with additional provisions tailored to the unique financial challenges faced by these individuals.

Choosing the most suitable type of bankruptcy depends on various factors, including your income, assets, debts, and long-term financial goals. It is crucial to consult with a bankruptcy attorney who can assess your situation and guide you through the process.